Sleep Number: New CEO Has Identified Challenges; Interesting Times Ahead

Sleep Number stock has struggled after the company's growth story started showing cracks. The new CEO is finally trying to address the challenges.

When I first came across Sleep Number Corporation (SNBR), the company behind the most advanced smart beds in the United States, I immediately fell in love with its story. This was in 2018. I even invested a small amount in SNBR stock, and to my delight, SNBR reached astronomical highs of close to $150 in 2021 before it all came crashing down. I exited Sleep Number with a nice profit, but back then, I was even contemplating whether booking my gains was the right course of action given the long growth runway. In hindsight, I have done well to book my gains, but I am deeply concerned by the wrong turns the company has taken since then, which have resulted in the company losing almost three-fourths of its market value in the last five years.

The smart bed industry has come a long way in the last few years, which makes Sleep Number’s fall even more concerning. The company’s newly appointed CEO Linda Findley offered some answers to the reasons behind its lackluster financial performance during the first-quarter earnings call. Even more importantly, she laid down her strategic response to overcome some of these challenges and steer the company back into growth mode in the future. With discretionary spending at risk, I highly doubt Sleep Number returning to growth this year, but I am encouraged by the new CEO’s understanding of the underlying reasons behind Sleep Number’s fall.

At Beat Billions, we keep a close eye on small-cap stocks with turnaround potential. While Sleep Number does not immediately qualify as one, I can see many reasons to keep a close eye on the company while it enters a transformative (and potentially painful) business phase.

Smart Beds Rise While Sleep Number Stumbles

The bedding industry has come a long way in the past decade, with the smart bed category showing disruptive potential. If you are not familiar with smart beds, these high-tech beds offer unique features such as adjustable mattress firmness, sleep tracking, climate control, and even smart home connectivity. Despite the stellar growth of the industry, Sleep Number has experienced a concerning trend of declining revenue. This presents a paradox worth exploring.

According to Fortune Business Insights, the global smart bed market was valued at $3.44 billion in 2024 and is on track to grow at a CAGR of almost 8% through 2032. So far, residential smart bed sales have fueled industry growth, but increasing demand for commercial usage (for example, in hospitals) is expected to drive the next wave of demand.

Exhibit 1: Smart bed market statistics

Source: Fortune Business Insights

The increasing awareness of the importance of high-quality sleep is at the center of demand growth for smart beds. Studies highlighting the impact of poor sleep on daily activities (affecting potentially 45% of Americans, per one study cited by MRFR) fuel demand for solutions offering tangible sleep quality improvements. Recent growth in sleep-focused wearables such as Whoop (I use a Whoop myself to improve my badminton performance) is also a testament to the growing interest in sleep performance.

The proliferation of smart homes provides fertile ground for smart beds as well. Global smart home penetration surpassed 13% in 2022, and we can only expect smart home penetration to rise in the future as the world embraces a more connected environment. Smart beds integrate into this ecosystem naturally, offering convenience and enhanced control over the sleep environment.

Innovations in sensors, IoT connectivity, and AI that enable sophisticated features like biometric tracking (heart rate, respiration), automated environmental adjustments (temperature, firmness), and personalized sleep coaching insights are also driving the demand higher for smart beds.

Although this may not be straightforward, I believe the growing aging population will also contribute to the growth of the smart bed market. I believe elder care facilities and hospitals will continue to embrace smart bed technology to improve their monitoring capabilities while providing care for the elderly population.

North America currently is the largest market for smart beds, accounting for around 60% of the global share. However, the Asia-Pacific region is often cited as the fastest-growing market, fueled by urbanization and rising disposable incomes.

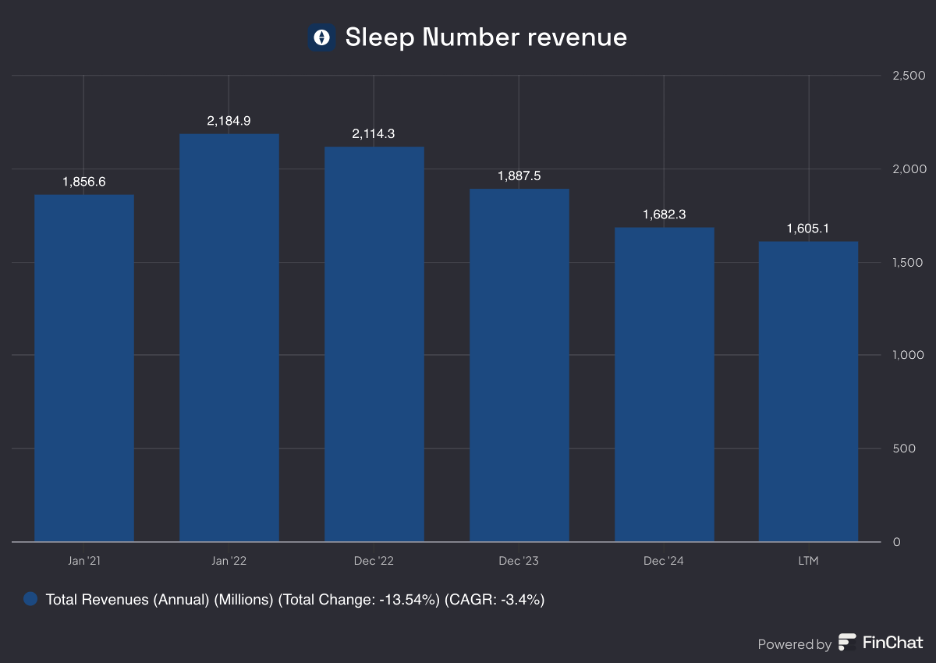

Despite operating within this promising industry landscape, Sleep Number's recent financial trajectory tells a different story. The company's annual net sales have contracted for three consecutive fiscal years:

Fiscal 2022: $2.11 billion (down 3.25% YoY)

Fiscal 2023: $1.89 billion (down 10.74% YoY)

Fiscal 2024: $1.68 billion (down 10.86% YoY)

Exhibit 2: Sleep Number revenue

Source: FinChat

This trend continued into the first quarter of fiscal 2025 as well, with a reported 16.4% year-over-year revenue decline. This divergence from the broader industry growth narrative suggests Sleep Number has faced significant company-specific challenges.

In an environment where consumers scrutinize large purchases, a potential misalignment between Sleep Number's product features, pricing tiers, and the perceived value by the target consumer could hinder sales. I believe this has been one reason behind the revenue decline. An overemphasis on high-end technological features might not have resonated sufficiently with budget-conscious consumers, or the benefits of these features may not have been communicated effectively enough to justify the premium price compared to "good enough" alternatives.

Sleep Number’s lack of marketing efficiency, as confirmed by the new CEO (more details later), is likely to have played a part in the poor performance too.

Sleep Number relies heavily on its own retail store network (around 637 locations as of Q1 2025). While offering brand control, this DTC model carries significant fixed operating costs. Declining foot traffic or conversions, reflected in falling same-store sales (averaging -1.9% annually over the two years prior to Q1 2025, with a sharper Q1 drop), puts direct pressure on profitability and makes deleveraging fixed costs difficult when revenue falls.

In summary, while the smart bed industry benefits from compelling long-term growth drivers, Sleep Number's recent financial performance indicates it hasn't fully capitalized on these trends. Although macroeconomic factors have played a role recently, the company’s struggles are largely due to company-specific challenges. Addressing these company-specific factors is critical for Sleep Number to realign its performance with the underlying potential of the smart sleep market.

The New CEO Sheds Light on Sleep Number’s Struggles and Path Forward

Sleep Number recently welcomed Linda Findley as the President and CEO of the company. Findley stepped onto the Q1 2025 earnings call not just to discuss quarterly results, but to lay out her vision for a significant turnaround. For investors scouting small-cap opportunities, understanding such pivotal moments is key. Let's break down the new CEO's assessment of the problems, the actions being taken, and what this could mean for Sleep Number's future. In full disclosure, I am not suggesting that Sleep Number stock is a good contrarian bet today at a time when Mr. Market has been looking down on the company. It seems too early to do that, but the first step is to understand the new CEO’s vision for the business.

A refreshing aspect of Findley's address during the Q1 earnings call was her candid acknowledgment of past strategic errors. She said:

"In the past, we got ahead of ourselves and the consumer."

This, in her view, led to a critical deviation:

"We focused on innovating so far into the future, and we lost sight of our core value proposition, helping people get a great night of sleep tonight."

This admission sets the stage for a back-to-basics approach, at least in terms of customer communication and immediate product focus. Findley elaborated on this during the Q&A, explaining:

"I think that we have maybe gotten a little bit further away from really explaining the value of the core Sleep Number proposition to the customer and making sure they just understand they're going to sleep better. Like that is just the truth."

This indicates a shift from potentially overwhelming consumers with complex features to clearly articulating the fundamental benefits of a Sleep Number bed.

Findley outlined a comprehensive plan, emphasizing that the company's challenges are "fixable in time and the solutions are largely within our control." She stressed a need to be "customer-obsessed" and is driving change with a heightened sense of urgency.

Here are the core pillars of her turnaround strategy:

Streamlining the organization for speed and efficiency: Findley's first priority is "to change the way we are organized for maximum efficiency and to bring us closer to our customer." This involves:

A new executive and senior leadership structure designed to consolidate overlapping capabilities and eliminate overspecialized roles. This has already led to a significant 21% reduction in corporate management.

Centralizing technology teams and driving end-to-end supply chain efficiencies. The goal, she explained, is to simplify decision-making, increase accountability and remove redundancies to better position us to succeed. This streamlined structure, she believes, will also improve the company’s ability to function quickly and innovate quickly because people will have clearer authority and the ability to make decisions faster.

Reinventing marketing: doing more with less (for now): With consumer sentiment expected to remain soft, the marketing approach is undergoing a significant overhaul. Findley sees a huge amount of opportunity for new efficiency in marketing with the goal of establishing a new marketing model that delivers more customer engagement from fewer dollars.

This means a shift towards new digital strategies and benefits-focused messaging designed for our target audiences.

The new CMO, Amber Minson, is tasked with driving sustainable demand generation, brand visibility and media efficiency to fuel growth.

Findley emphasized a temporary focus on efficiency: "We plan to reinvest in marketing when the time is right. But for now, our focus is on doing more with less." When asked about potential negative sales impact from reduced marketing spend, Findley highlighted a strategic rethink: "We're not looking at it from a term of just cutting. We're actually looking at it from a term of reset and thinking about how we also leverage our digital property...to help drive additional efficiency so we can deviate from some of the trends of the past where a cost cut would actually automatically result in a lower customer number."

Refocusing R&D on core strengths and customer needs: While Sleep Number was built on innovation, and it will continue to be so, the approach is being refined. "It's essential that we strike the right balance between enhancing innovation and ensuring that shareholder capital is being used efficiently."

The plan is to deprioritize adjacent opportunities where returns are uncertain or will take longer to realize.

Instead, resources will focus on "maintaining and improving our core technologies and introducing additional advancements while driving costs out of the product." Findley believes the company's vast sleep data ("33 billion hours...and counting") provides a significant advantage, allowing them "to focus our resources on the here and now of our customers' needs."

Aggressive cost reduction: A significant financial target accompanies these strategic shifts. The company expects "the collective actions to reduce expenses by about $80 million to $100 million before restructuring costs on an annualized basis as compared to the Q1 2025 cost structure. CFO Francis Lee noted that approximately 35% of these are fixed costs (R&D, G&A), 50% are structural changes to marketing, and 15% are volume-driven. Immediate action has been taken, as Findley revealed, "we have already reduced our Q2 operating expenses by approximately 10% compared to the Q1 2025 cost structure."

Beyond these initial actions, Findley signaled a deeper, more fundamental review of the business. This holistic review will scrutinize:

Supply chain

Distribution strategy (including a potential re-evaluation of wholesale, a point raised by an analyst)

Product selection

Geographic reach

Partnerships

When questioned about wholesale distribution, Findley reiterated, "All I can say is our eyes are very, very fresh and everything is on the table.” This open-minded yet decisive approach suggests that more significant structural changes could be on the horizon.

Takeaway

Sleep Number is a company that I have always kept a close eye on. Unfortunately, the company is currently facing significant challenges. The new CEO, encouragingly, has identified these challenges and has come up with a preliminary strategy to address them. I believe the next few quarters will be interesting for the company and its shareholders, and I will keep a close eye to identify potential inflection points.

Disclaimer: This article is for informational purposes only and should not be considered investment advice. The opinions expressed are those of the author based on current market conditions and publicly available information. Sleep Number Corporation and its financial performance may be subject to various risks and uncertainties. Investors should conduct their own due diligence or consult with a qualified financial advisor before making any investment decisions. The author and Insights Terminal do not hold any responsibility for investment actions taken based on this content.

Disclosure: I do not own any stocks mentioned in this article.